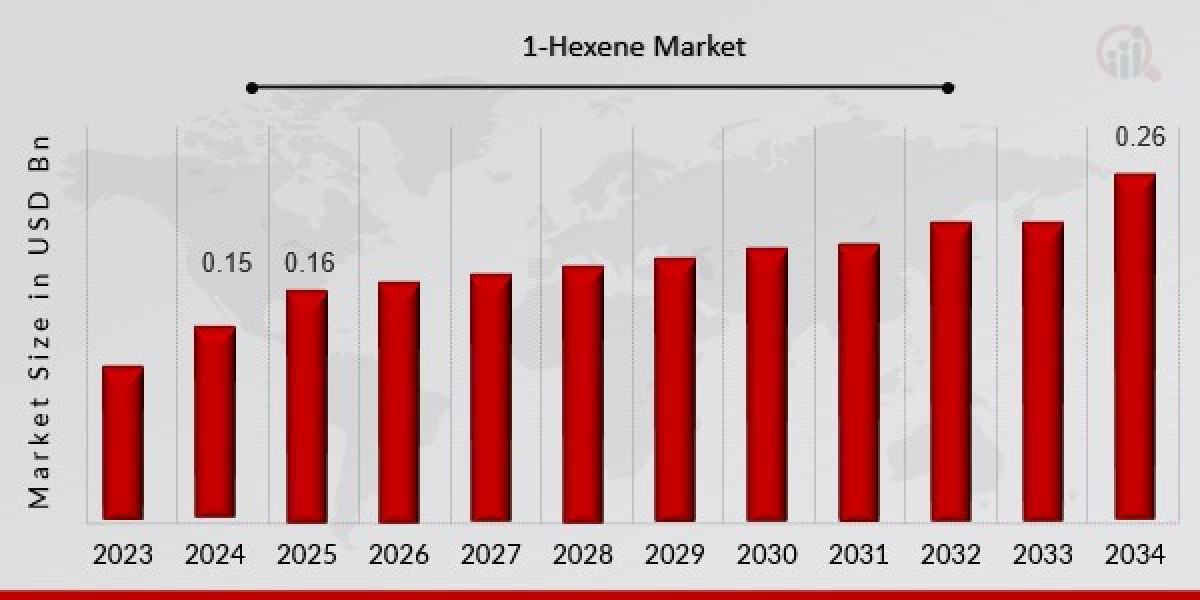

The 1-Hexene market has been steadily expanding in recent years, driven largely by its critical role in the production of polyethylene, particularly linear low-density polyethylene (LLDPE). This compound, an alpha olefin with the formula C₆H₁₂, is widely used as a comonomer in polyethylene manufacturing processes. The rising global demand for plastic packaging, industrial films, and consumer products has created a sustained need for 1-Hexene, making it an integral part of the petrochemical value chain.

Polyethylene made using 1-Hexene demonstrates enhanced strength, flexibility, and durability. These qualities are especially valuable in industries such as packaging, automotive, agriculture, and construction. As economies around the world continue to industrialize and urbanize, the demand for efficient and lightweight materials like LLDPE has surged. This, in turn, supports the growth of the 1-Hexene market. One of the significant applications of 1-Hexene lies in the packaging sector, which consumes large quantities of plastic films and containers. The e-commerce boom and the increasing preference for pre-packaged goods have further amplified this demand.

The production of 1-Hexene is commonly carried out through processes such as ethylene oligomerization and the Fischer-Tropsch synthesis route. Among these, on-purpose production methods — those specifically designed to yield 1-Hexene rather than as a byproduct — are becoming more widespread. Companies are investing heavily in these advanced production techniques to improve efficiency and maintain consistent supply. This has also led to the growth of dedicated facilities, particularly in regions with abundant feedstock availability such as North America and the Middle East.

North America has emerged as a leading player in the global 1-Hexene market due to its rich reserves of natural gas and shale gas, which are converted into ethylene. This ethylene serves as the primary input for 1-Hexene production. In the United States, companies like Chevron Phillips Chemical and INEOS have built large-scale facilities that cater not only to domestic needs but also export to markets in Asia and Europe. The integrated nature of the petrochemical industry in North America makes it a cost-effective and reliable region for the production of alpha olefins like 1-Hexene.

Asia-Pacific, on the other hand, is witnessing the fastest growth in consumption. Countries like China, India, and South Korea are experiencing increased industrial output and rapid urban development, leading to higher demand for plastics and related products. The rise in infrastructure projects, construction activities, and automotive manufacturing has created a surge in the use of LLDPE and other polyethylene variants that incorporate 1-Hexene as a key raw material. Manufacturers in these countries are also scaling up their operations, often through joint ventures and technology partnerships with Western firms.

Europe represents a mature but environmentally progressive market. The region’s focus on sustainability and regulations around plastic use have created a dual effect — while demand for traditional plastics faces scrutiny, there is increasing innovation in the use of recyclable and eco-friendly polymers. 1-Hexene continues to play a role in these new formulations, especially as the industry explores materials that retain performance while meeting regulatory compliance. European producers are also investing in research to reduce the environmental impact of 1-Hexene production, including exploring bio-based alternatives.

The automotive industry, too, is a significant contributor to the 1-Hexene market. Lightweight plastics are essential for improving fuel efficiency and meeting strict emission norms. With the transition toward electric vehicles, there's a growing need for high-performance materials that can offer thermal resistance, strength, and durability. 1-Hexene-derived plastics are increasingly being used in the interiors, under-the-hood components, and external trims of modern vehicles.

On the competitive front, the 1-Hexene market is relatively consolidated, with a few multinational corporations controlling a significant share of global production. These companies leverage advanced technologies, strategic geographical positioning, and extensive distribution networks to maintain their market dominance. Research and development are focused on process optimization, reducing production costs, and improving the quality of output to meet evolving industry requirements.

Sustainability is becoming a central theme in the 1-Hexene market. With mounting pressure to reduce the environmental footprint of petrochemical processes, manufacturers are exploring greener production routes, energy-efficient systems, and waste reduction techniques. There is also an emerging interest in renewable and bio-based feedstocks that could serve as alternatives to traditional hydrocarbon sources, although these solutions are still in early stages of commercialization.

In terms of challenges, the 1-Hexene market faces volatility in raw material pricing, logistical disruptions, and stringent environmental regulations. Crude oil and natural gas prices directly affect the cost of production, while supply chain issues can lead to inconsistent delivery and planning difficulties for end-users. Regulatory compliance, particularly in the European Union and North America, adds additional layers of complexity that producers must navigate.

Despite these challenges, the future of the 1-Hexene market looks promising. Continuous innovation, growing global demand for high-performance plastics, and increasing investments in downstream applications are expected to sustain the market's momentum. As industries adapt to changing economic and environmental conditions, 1-Hexene will continue to serve as a foundational building block for a broad array of modern materials and applications.